Ratio Spread Strategy

- What is a Ratio Spread?

- Understanding Front and Back Ratio Spreads

- Directional Assumptions in Ratio Spreads

- Core Mechanics of Ratio Spreads

Spreads are often considered the foundation of many multi-leg option strategies. They are relatively simple to construct and offer defined risk and reward, making them a practical tool for traders.

There are two basic types of spreads:

Credit Spreads, where the trader receives a net premium

Debit Spreads, where initiating the trade requires a cost

A Ratio Spread is an advanced extension of the basic spread strategy. It introduces a directional outlook and offers a high probability of favorable returns under the right market conditions. Let’s delve deeper into the nuances of this strategy.

What is a Ratio Spread?

A Ratio Spread is an options trading strategy involving both long and short positions of the same type, either calls or puts, but in unequal quantities. The strategy is designed to capitalise on directional price movement with a built-in risk-reward framework.

A common structure is the 2:1 ratio, where two options are sold for every one option purchased. This approach can convert the strategy into a credit trade, where the premium from the additional short option offsets the cost of the long option.

Ratio spreads can be categorized into:

Front Ratio Spreads: More short options than long

Back Ratio Spreads: More long options than short

Front Ratio Spreads

A Front Ratio Spread starts as a standard debit spread and is modified by adding an extra short option at the same strike as the existing short leg. This changes the strategy into a net credit spread.

Example (Call Front Ratio Spread):

Buy 17,700 Call

Sell two 17,750 Calls

This configuration eliminates downside risk and introduces a capped profit zone if the price closes near the short strike (17750). The strategy benefits from a moderately bullish outlook.

If the market rallies beyond the breakeven, profit starts diminishing and losses can mount beyond a certain level.

Example (Put Front Ratio Spread):

Buy an ATM Put

Sell two OTM Puts

This structure introduces a mild bearish bias and creates a credit strategy. The maximum profit occurs if the underlying closes near the sold strike. Losses are limited on the upside.

Greeks Insight:

Call Front Ratio: Starts with a negative delta and profits if the price moves down to the short strike

Put Front Ratio: Starts with a positive delta and profits if the price rises toward the short strike

Directional Assumptions

Front Ratio Spreads are often seen as directionally flexible strategies when structured for a credit. Here’s how directional bias plays out:

Put Front Ratio:

• Positive delta

• Profits on a downward move

• No risk on the upsideCall Front Ratio:

• Negative delta

• Profits on an upward move

• No risk on the downside

Maximum gains are achieved when the stock closes right at the short strike on expiry.

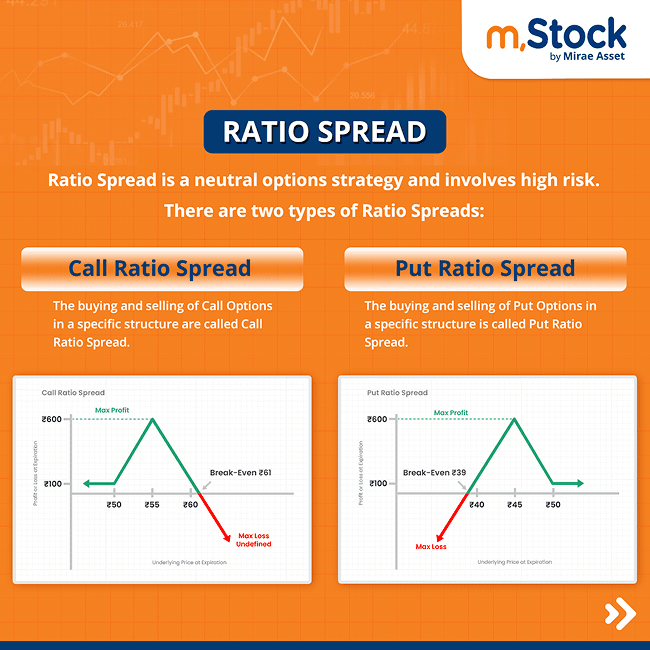

Ratio Spread Dynamics

Traders typically employ Ratio Spreads when expecting the market to stay within a moderate price range, with a slight directional lean based on the type of option used:

Slightly Bullish View: Use Call Ratio Spread

Slightly Bearish View: Use Put Ratio Spread

In a 2:1 setup, only one short option is hedged by the long position. This leaves the second short option uncovered, exposing the trader to unlimited loss potential beyond the breakeven range.

Maximum Profit = (Difference between strike prices) + Net credit

Maximum Loss = Theoretically unlimited beyond breakeven (if price moves aggressively in one direction)

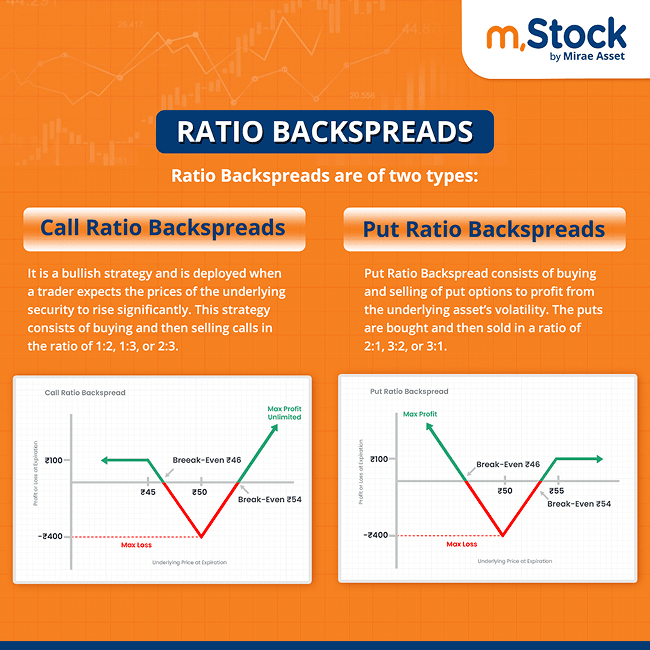

Back Spread

A Ratio Back Spread takes the opposite approach: it involves buying more options than selling. It is used when the trader has a strong directional view bullish or bearish based on the type of option used.

Call Back Spread: Constructed for bullish market moves

Put Back Spread: Constructed for bearish expectations

This strategy allows for unlimited gains in the direction of the trade and a limited loss if the market remains stagnant.

Call Backspread

Structure:

Sell one ATM or ITM Call (e.g., 17,650)

Buy two OTM Calls (e.g., 17,750)

The net effect usually results in a credit, offering the potential to earn if the market moves significantly higher. If the market dips, a small profit is still possible, but the worst-case loss occurs if it stagnates near the strike of the long calls.

Put Backspread

Structure:

Sell one ATM or ITM Put (e.g., 17650)

Buy two OTM Puts (e.g., 17500)

This strategy benefits from sharp downside moves. The credit received at the time of trade setup cushions minor upward moves. The maximum loss is confined to a narrow range around the long Put strike.

Backspread Dynamics

A Backspread is designed for explosive market moves. The standard ratio is 2:1 (buying two options for every one sold). Based on the options selected:

Call Backspread: Used for bullish sentiment

Put Backspread: Used for bearish expectations

This strategy is the inverse of a Front Spread. Instead of generating income through excess short positions, the Backspread aims for asymmetrical reward potential, betting on volatility and large price swings.

Conclusion

Spreads are the cornerstone of many options strategies, providing a mix of defined risk and reward.

Ratio Spreads an advanced adaptation—build upon basic debit spreads.

Front Spreads: More options are sold than bought (commonly 2:1), generating credit and directional exposure.

Backspreads: More options are bought than sold (commonly 2:1), providing limited loss and unlimited profit potential in the trade's direction.