Long and Short Iron Condor: All You Need to Know

- Understanding the Long Iron Condor strategy and how to construct it

- Key differences between Long and Short Iron Condor strategies

In the evolving landscape of Indian options trading, strategies like the Iron Condor are gaining momentum especially following the regulatory shifts in margin requirements. Unlike Straddle and Strangle, which are two-legged setups, the Iron Condor is a more complex four-legged strategy, offering delta-neutral exposure with limited risk and reward.

The Iron Condor merges bullish and bearish vertical spreads to form a non-directional outlook, aiming to profit from specific market behaviors.

At m.Stock, understanding such strategies can help you better navigate different market scenarios with calculated risk.

What Is an Iron Condor?

The Iron Condor gets its name from the wide spread of its strike prices—much like the wingspan of a condor. This strategy is delta-neutral, constructed using:

2 Call Options (one long, one short)

2 Put Options (one long, one short)

All options share the same expiry and underlying asset but are placed at different strike prices.

There are two types:

Long Iron Condor (Net Debit Strategy)

Short Iron Condor (Net Credit Strategy)

Let’s explore both strategies in detail.

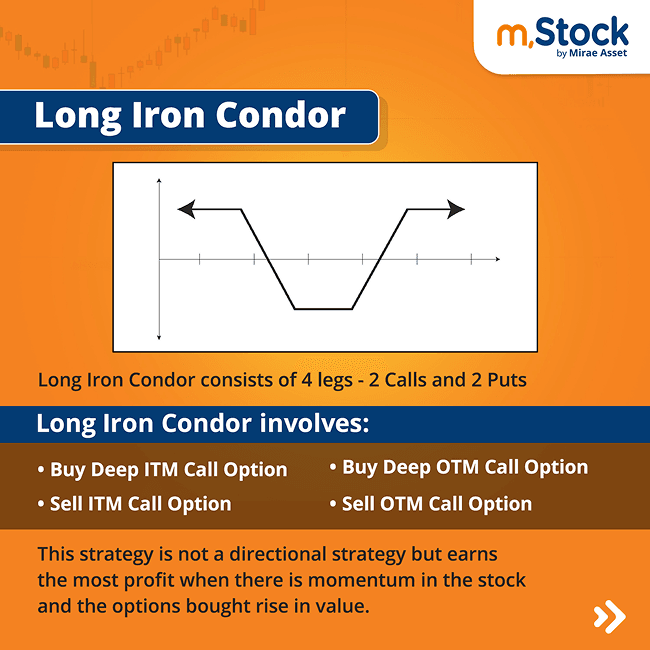

Long Iron Condor

The Long Iron Condor is a net debit strategy, meaning the trader pays a net premium to establish the trade. This strategy involves buying two inner strike (OTM) options and selling two outer strike (further OTM) options, both on the call and put side.

It is best suited for traders who expect a significant move in either direction, and increased volatility.

Strategy Setup

All options are out-of-the-money (OTM):

Sell 16,700 Put @ ₹81

Buy 17,100 Put @ ₹146.90

Sell 18,650 Call @ ₹32.35

Buy 18,250 Call @ ₹102

This forms a combination of a Put Debit Spread and a Call Debit Spread.

Trade Details

Underlying: Nifty

Expiry: 29th September

Margin Requirement: ₹35,118

The strategy is loss-making if the market stays between the two sold strikes, and profitable only if the price breaks out beyond the breakeven levels.

Calculations

Net Debit = ₹81 + ₹32.35 – ₹146.90 – ₹102 = ₹135.55

Total Debit (Loss Potential) = ₹135.55 × 50 = ₹6,777.50

Max Profit = ₹17,100 – ₹16,700 – ₹135.55 = ₹264.45

Max Profit in ₹ = ₹264.45 × 50 = ₹13,222.50

Lower Breakeven = ₹16,700 + ₹264.45 = ₹16,964.45

Upper Breakeven = ₹18,250 + ₹135.55 = ₹18,385.55

Summary

Created in high volatility environments

Requires a strong price move in either direction

Defined risk and defined profit

Time decay (theta) works against the strategy

Delta-neutral by construction

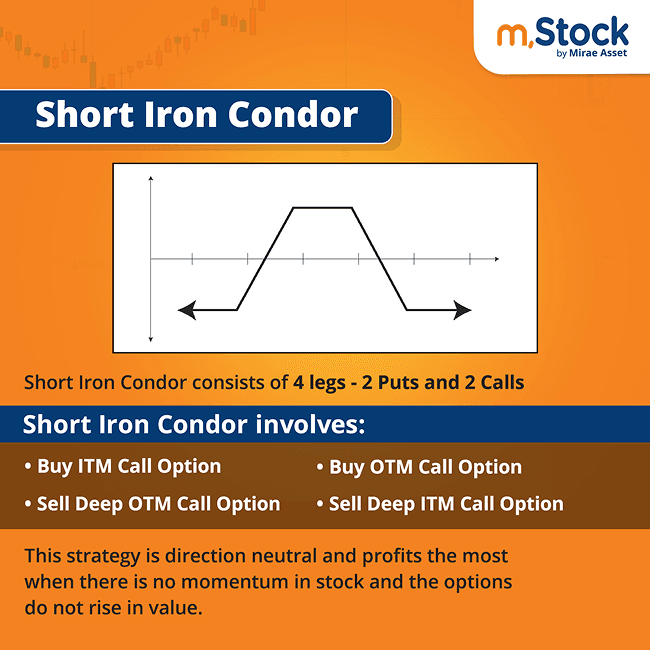

Short Iron Condor

The Short Iron Condor is the opposite of the long variant. It is a net credit strategy, where the inflows from the sold options exceed the cost of the long options. This setup is preferred when the trader expects the market to remain range bound.

Traders use this strategy to benefit from time decay, especially when implied volatility is expected to fall.

Strategy Setup

All options are out-of-the-money (OTM):

Buy 16,700 Put @ ₹81

Sell 17,100 Put @ ₹146.90

Buy 18,650 Call @ ₹32.35

Sell 18,250 Call @ ₹102

This structure combines a Put Credit Spread and a Call Credit Spread.

Trade Details

Underlying: Nifty

Expiry: 29th September

Margin Requirement: ₹52,198

This strategy is profitable when the market stays within the two sold strikes, and losses occur if the price breaches breakeven levels on either side.

Calculations

Net Credit = ₹146.90 + ₹102 – ₹81 – ₹32.35 = ₹135.55

Total Credit (Profit Potential) = ₹135.55 × 50 = ₹6,777.50

Max Loss = ₹17,100 – ₹16,700 – ₹135.55 = ₹264.45

Max Loss in ₹ = ₹264.45 × 50 = ₹13,222.50

Lower Breakeven = ₹16,700 + ₹264.45 = ₹16,964.45

Upper Breakeven = ₹18,250 + ₹135.55 = ₹18,385.55

Summary

Profits from a sideways or range-bound market

Theta decay works in favor of the strategy

Ideal for use when volatility is high and expected to drop

Defined profit and defined risk

Widely used for intraday and earnings-related trades