Calendar and Double Calendar Spreads

- Understanding Calendar Spreads

- Types of Spreads: Vertical, Horizontal, and Diagonal

- Ideal Conditions for Calendar Spreads

- Strategic Benefits of Calendar Spreads

Options spreads are typically composed of two legs. The strategy name depends on how these legs are positioned.

There are three commonly used spread types:

Vertical Spreads involve two options of the same expiry but different strike prices.

Horizontal Spreads (or Time Spreads) use options of the same strike but different expiries.

Diagonal Spreads combine both – different strikes and different expiries.

In this post, our focus will be on Calendar Spreads, a type of horizontal spread using options with identical strikes but different expiration dates.

A quick note: There is also a futures-based version of the calendar spread strategy. This involves buying a cheaper future and shorting a costlier one of the same underlying, aiming to profit when the price difference narrows.

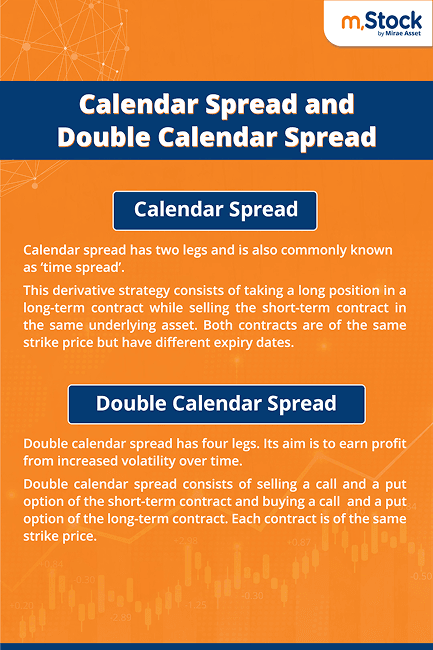

What is a Calendar Spread?

A Calendar Spread involves a long and short position in options of the same strike but with different expiry dates.

The long leg is taken in a far expiry.

The short leg is placed in a near expiry.

For example, in a Nifty calendar spread:

Sell 17350 Call Option (near expiry – 13th October)

Buy 17350 Call Option (far expiry – 27th October)

This is a debit spread strategy, where the premium paid exceeds the premium received. It can be executed using either Call or Put options.

When Should You Use a Calendar Spread?

This strategy is best suited when the market is expected to remain range-bound or move slightly in either direction.

A Calendar Spread is typically used:

In low implied volatility environments

When expecting volatility to rise after trade entry

To profit from time decay on the short leg

With a mild bullish or bearish view

If you expect slight upward movement, sell an OTM call for the near expiry and buy the same strike for the far expiry.

Why Traders Use Calendar Spreads

The profitability of a calendar spread is rooted in time decay and volatility:

Near-term options decay faster

Long-term options retain more extrinsic value

Rising implied volatility benefits the long option

These spreads are typically created using ATM (at-the-money) options for maximum sensitivity.

Capital efficiency is another major advantage. In the earlier Nifty example, margin required was just ₹22,357, while return on investment can touch ~23%, significantly higher than typical vertical spreads.

Risk: What Is the Maximum Loss?

Since calendar spreads are debit strategies, maximum loss is limited to the net premium paid.

Example Calculation:

Sell 13Oct 17350 CE at ₹121.95

Buy 27Oct 17350 CE at ₹274.10

Net debit = ₹152.15

Total loss = ₹7,607.50 (for 1 lot of Nifty)

Maximum gain occurs when the price closes near the short leg at expiry. If volatility rises, the far option retains value, increasing profit.

Understanding Double Calendar Spreads

A Double Calendar Spread is created by combining two calendar spreads:

One below the market (Put)

One above the market (Call)

This strategy is best deployed when volatility is low and expected to rise.

What is a Double Calendar Spread?

A Double Calendar Spread involves:

Selling near-term Calls and Puts

Buying far-term Calls and Puts (same strike, same underlying)

This is a debit strategy that profits from rising volatility (positive Vega). Typically, the ratio is 1:1 for each leg.

Payoff Diagram & Practical Example

The payoff graph of a Double Calendar shows two profit peaks, one each at the sold call and put strikes.

Example:

Upper Leg: Sell 08 Dec 18900 CE & Buy 29 Dec 18900 CE

Lower Leg: Sell 08 Dec 18500 PE & Buy 29 Dec 18500 PE

This setup creates a “tent” of profitability. The market must stay within this range to maintain gains. Margin requirement in this example: ₹48,261. Probability of profit: 71.2%.

When Should You Trade a Double Calendar Spread?

Ideal conditions to enter a Double Calendar Spread:

Low-volatility environments

Ahead of key events (e.g., RBI policy meetings)

The structure benefits from rising implied volatility in the far expiry while the near-term options decay quickly.

A good trade setup appears when:

Near expiry IV > Far expiry IV

Market is expected to stay within a narrow band

Difference between Calendar Spread and Double Calendar Spread

As seen from their construct, while a calendar spread requires buying and selling of either a call or put option of two different expiries, a double calendar spread requires both calls and puts of two expiries for its construction.

Compared to the calendar spread, which is a two-legged strategy, a double calendar spread is a four-legged strategy.

The double calendar spread normally covers a wider space as the trade can be profitable if the price remains between the two tents. With the same premiums, a calendar spread trade will cover a smaller area.

Effectively, a double calendar spread combines a short strangle in the near expiry and a long strangle in the far expiry. On the other hand, a calendar spread is a combination of a short call or put and a long call and a put of different expiries.

Conclusion

Calendar and Double Calendar Spreads are ideal for traders operating in range-bound markets with a view on implied volatility.

Calendar spreads offer low capital requirement and strong ROI potential

Double calendars provide a broader profit range but at a slightly higher cost

Both strategies benefit from time decay and rising volatility

m.Stock offers robust tools to execute these trades efficiently, giving traders an edge in dynamic markets.